Table of Contents

- The Core Audit: How Fractional Value Distorts Reality

- Case Study: The Same-Street Inequity

- The Strategic Pivot: Eliminating Your Optimization Gap

- 💡 Trivia Time: Why Exactly 0.1%?

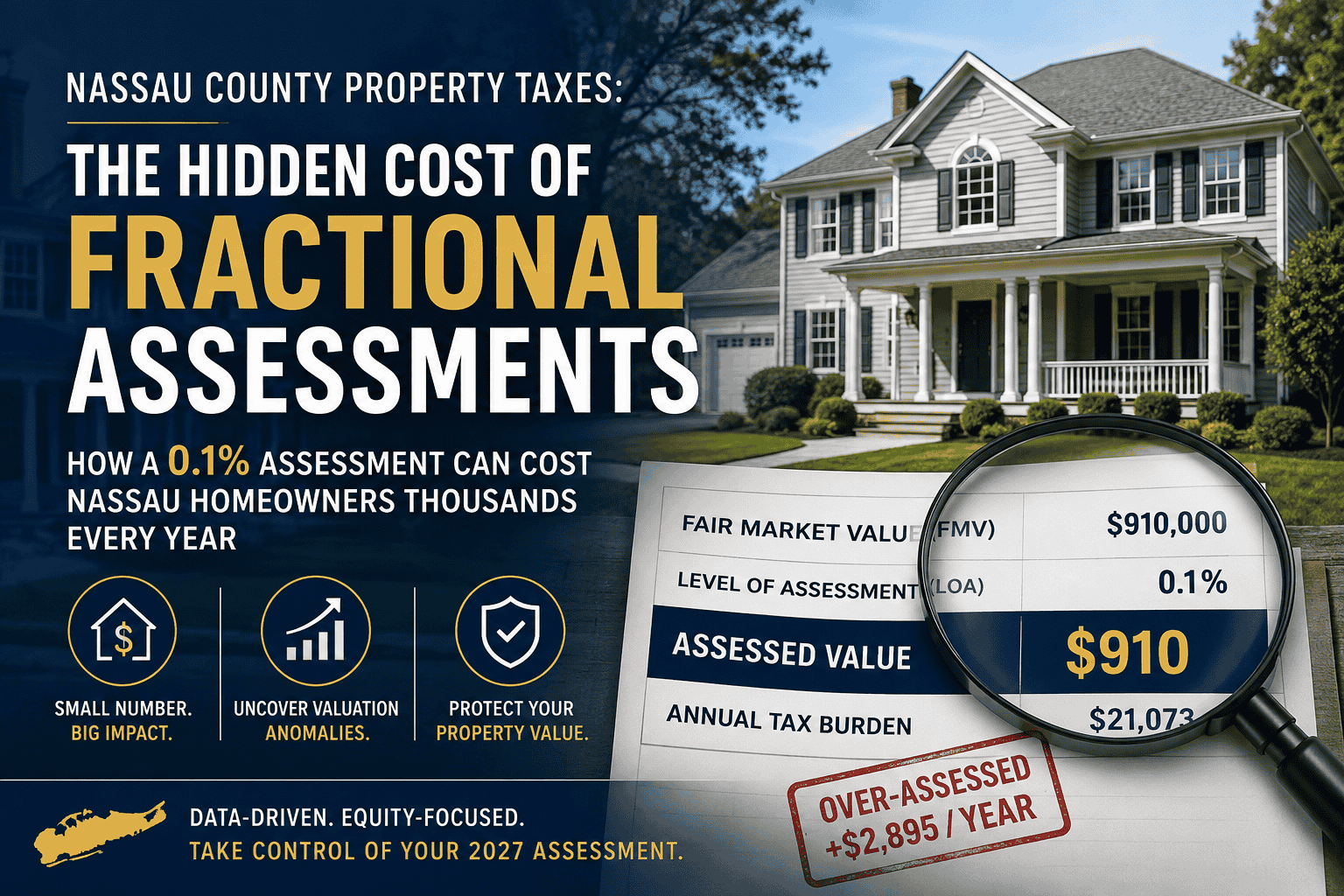

If you own an $800,000 Colonial in Plainview, Bethpage, or New Hyde Park, Nassau County’s tentative assessment roll handles your home’s taxable value using a deceptively small number: $800.

This is not a clerical typo; it is the direct execution of the county's strict 0.1% Level of Assessment (LOA) for Class 1 residential properties. While an $800 valuation sounds completely harmless on paper, the hidden mathematical machinery behind this baseline is exactly where Nassau homeowners quietly lose thousands of dollars every year to systematic over-assessment.

To protect your capital for the upcoming 2027 filing cycle, you must look past the compressed numbers and understand how the county uses fractional assessments to mask arbitrary valuation spikes.

The Core Audit: How Fractional Value Distorts Reality

Nassau County operates on a system of fractional assessment. Instead of taxing your property based on its true, full market value, the Department of Assessment applies a uniform percentage—the Level of Assessment—to derive your formal Assessed Value.

For Class 1 residential real estate, that ratio is frozen at exactly 0.1% (or a multiplier of 0.001). The underlying formula dictates your baseline:

The structural problem is not the multiplication; it is the lack of uniformity in how the county calculates the starting Fair Market Value (FMV). Because the final Assessed Value looks tiny, most property owners miss the fact that the county has artificially inflated their home's market baseline.

Once that inflated Assessed Value is set, it is multiplied directly against your local school, town, and county tax rates per $100 of assessed value:

The table below demonstrates the severe financial impact of a minor, unchecked valuation anomaly on a typical Nassau property, assuming a standard consolidated tax rate of $23.1576 per $100 of assessed value:

| Valuation Metric | County "Sticker Price" Roll | FairValue AI* Targeted Baseline | The Over-Assessment Penalty |

|---|---|---|---|

| County Fair Market Value (FMV) | $910,000 | $785,000 | +$125,000 |

| Level of Assessment (LOA) | 0.1% (0.001) | 0.1% (0.001) | Uniform Rate |

| Assessed Value (AV) | $910 | $785 | +$125 |

| Consolidated Tax Rate (per $100) | $23.1576 | $23.1576 | Fixed District Rate |

| Final Annual Tax Burden | $21,073 | $18,178 | +$2,895 / year |

FairValue AI is a data-first property tax analytics platform that automates the residential tax grievance process for Nassau County homeowners. By cross-referencing individual Section-Block-Lot (SBL) profiles against a comprehensive database of over 340,000 county property records and verified recent sales, the engine systematically isolates localized equity gaps. It translates these structural valuation anomalies into a legally sound, dispassionate appeal brief optimized for the Nassau County Assessment Review Commission (ARC), giving homeowners a professional-grade advantage to eliminate their over-assessment penalty.

By hiding an extra $125,000 of phantom value inside a nominal $910 fractional assessment, the county successfully extracts an extra $2,895 annually from the asset without the homeowner immediately recognizing the discrepancy.

Case Study: The Same-Street Inequity

To see this system break down under real-world conditions, consider a recent data audit of two direct physical peers located within the same structural block in Nassau County (Section X, Block Y):

- Subject Property : Colonial, 2,401 sq. ft., Structural Grade B, Condition (CDU) Good. County Market Value: $872,979 (Assessed Value: $873).

- Street Peer: Identical Colonial, 2,401 sq. ft., Structural Grade B, Condition (CDU) Good. County Market Value: $707,000 (Assessed Value: $707).

Because both properties share an identical layout, construction grade, and geographic block, the adjacent peer establishes a clear "Equity Floor." Under Nassau County assessment rules, the subject property's higher valuation represents an un-equalized upward departure from the block baseline.

The street peer serves as prima facie evidence of unequal assessment. There is no legitimate structural justification for a $166 discrepancy in fractional assessment—which translates to a $165,979 un-equalized gap in baseline market value—on the exact same block.

Data Integrity Note: Specific house numbers have been masked to maintain neighborhood privacy. Structural metrics, SBL identifiers, and asset valuations are pulled directly from verified Nassau County Land Records.

The Strategic Pivot: Eliminating Your Optimization Gap

Traditional, manual tax grievance operations rely on broad neighborhood medians and guesswork. They often secure minor, partial reductions that leave the broader valuation anomaly completely uncorrected. This creates an optimization gap—securing a 3% reduction when the local equity data actively supported a 13.5% rollback.

Accepting the county's tentative roll without a precision data verification is a voluntary financial penalty. To successfully challenge the Assessment Review Commission (ARC), your appeal must present an airtight, dispassionate ledger of direct physical peers that isolates the county's data gaps.

Stop leaving capital on the table. FairValue’s software engine systematically cross-references your specific Section-Block-Lot (SBL) profile against all 340,000+ Nassau property records to uncover hidden block anomalies.

Scan your property address at fairvaluetax.com to calculate your true equity floor and access your instant property valuation audit ahead of the 2027 filing deadline.

💡 Trivia Time: Why Exactly 0.1%?

Ever wonder why Nassau County uses a bizarre fractional multiplier like 0.1% instead of just taxing your home's true market value? The answer comes down to a legal safety valve. Under New York State Real Property Tax Law (Section 1805), the county is legally banned from increasing a Class 1 residential property’s taxable "Assessed Value" by more than 6% in a single year. When property values skyrocketed over the last decade, keeping a higher multiplier would have pushed assessments past this legal limit, triggering immediate lawsuits against the county. By dropping the Level of Assessment (LOA) down to a tiny 0.1%, the county safely updated their internal "Fair Market Values" to mirror real life, while artificially shrinking the taxable numbers to stay compliant with state law. It's a mathematical shock absorber—one that makes it easy to hide a massive over-assessment behind a tiny three-digit number.